The Current State of Digital Advertising

The Shifting of Attention, Regulation, and Social Media’s Evolution

One of the most impactful investment essays ever written was Increasing Returns and the New World of Business by Brian Arthur in 1996.

In it, Arthur observes that for a small handful of companies, they don’t see the decreasing returns that had been observed for several centuries, but increasing returns. The strong get stronger. The rich get richer.

If you had invested behind this one theory for the last 30 years, it’s been a very fruitful thirty years for you (outside of any catastrophic behavioral or leverage mistakes, of course).

For the last two decades, the digital advertising market has epitomized those increasing returns. Consolidating to a few, massive, power-lawed, network-driven, attention marketplaces. In that time, not only did they produce two of the largest IPOs ever, but they also achieved wonderful public returns.

Translated: Early on, people saw how incredible Google and Meta would be. The only thing they missed was just how incredible.

Now, however, the market’s at its most interesting point in a decade:

Attention is shifting as information retrieval fundamentally changes.

Regulators are looking to remove the advantages built up by digital ad networks over the last two decades.

Consumers are more immune to advertising, leading advertisers to pay most for the ability to influence buying decisions.

One of the harbingers of digital ads, social media, has fundamentally shifted from social media to media.

I can’t help but be deeply interested when there’s a massive industry facing the shifting sands of disruption.

With that, let’s get to it. This will be a deep dive on the digital advertising industry: its value chain, market statistics, and trends shaping the industry.

A Quick Primer on Digital Advertising

Given the profile of these businesses, I’ll keep the primer section short (and perhaps best explained in visual format below).

Broadly, we have a few categories that make up the advertising industry:

Walled Gardens like Meta, Google, Amazon, Tiktok that require you to go through their platform if you want to advertise with them.

Non-Walled Gardens include the rest of the channels that showing digital ads such as publishers like the Wall Street Journal, music providers like Spotify, mobile games, and streaming providers like Netflix.

Demand-Side Providers (DSPs): Platforms like the Trade Desk, that aggregate advertiser demand, to connect to ad exchanges/SSPs.

Supply-Side Providers (SSPs): Platforms like Google’s AdX (now integrated into Ad Managers) that aggregate advertising inventory from multiple publishers, connecting to various Demand-Side Platforms (DSPs).

Channel-Specific infrastructure: Platforms that provide an ad network to a specific vertical; AppLovin, for mobile gaming, is the best example of this.

Ad Agencies like WPP and IPG that build campaigns and manage advertisements for advertisers.

Publishers like the WSJ that sell ad inventory.

Supporting tooling like tooling to design ads (Canva, Adobe), analytics to track ROI (typically rolled up into an ad platform or CRM), and ad servers (store and place ads based on the ad auctions).

The Walled Gardens make up over 50% of the US digital ads market:

Three primary types of digital ads drive the walled gardens: search (consumers come for information), “social” media (consumers come for entertainment), and e-commerce (consumers come to buy).

The nature of these systems is built around accurately matching large amounts of supply and demand. What the supply and demand are varies by use case, but they could be content, ads, advertisers, or user preferences.

Regardless, these matching problems are a perfect use case for AI. Matching also needs to happen in real-time, meaning the hardware requirements for latency are quite high. Because of this, digital advertising essentially bankrolled the AI industry for the last decade. It was the most valuable application of AI, and funded the developments that have taken the world by storm over the last two years.

Outside of those walled gardens, the majority of spend goes through the “open web.” With that context, I see four trends driving the industry:

Regulation & Google Ad Network’s Decline

The Rise of E-Commerce Advertising: Increasing Consumer Ad Immunity and the Pursuit of ROI

The Shift from Social Media to Media

The Shifting of Attention in Search

Trend #1: Regulation & Google Ad Network’s Decline

Last week, Google was deemed a monopoly, specifically on the supply side of the “open web.”

This starts with Google Search. For advertisers to place ads on search, they need to go through Google Ads (formerly known as AdWords). Those open-web ads get placed through Google Ad Exchange.

Publishers, on the other hand, need access to that vast number of advertisers through Google Ad Platform. This includes ad servers, which store and place ads on ad inventory in real-time.

The argument from the DoJ was that Google unfairly tied these services together, specifically the ad server and the ad exchange. In doing so, they created a self-reinforcing loop for advertisers and publishers:

Advertisers needed to access publishers, which is done through Ad Exchange.

Publishers needed to access advertisers, which is done through Ad Exchange.

By tying together the ad server and the ad exchange, publishers were locked into the Ad Exchange. In turn, that locked both parties into the Ad Exchange, which locked them into the whole network.

I won’t comment on the unfair practices, but regardless, it led to a dominant flywheel of an attention marketplace. As publisher supply increased, so did advertiser supply, and vice versa. Google then leveraged those data advantages, and their AI prowess, to further cement their advantages.

That led to Google having the largest market share in North America in DSPs (see above), Ad Servers (the DOJ estimated Google had a 90% market share in ad servers), and SSPs.

On top of that, they have both data and existing relationships from advertisers needing access to both Search and Youtube.

With all those advantages, Google should have continued to get more dominant. And they did, for a while. However, over the last three years, that dominance has flattened:

Whether voluntarily or involuntarily, Google’s ad network has ceded share to competitors like the Trade Desk. This means the $30B+ open web ad market may be up for grabs, and Google’s ad network may get spun off from the parent company.

However, the more interesting implication is this: if Google's Ad Network gets broken up, could it create a Standard Oil-like effect on the digital ad network? Will Google’s Ad Network get a cool new name and be unlocked to fully leverage those advantages listed above?

Trend #2: The Rise of E-Commerce Advertising: Increasing Consumer Ad Immunity and the Pursuit of ROI

One other interesting ruling from the Google case was that advertisers are actually “agnostic” to the platform they advertise on, they just want ROI:

Substantial trial evidence showed that advertisers reallocate resources among different digital advertising channels based on perceived return on advertising expenditures (“Ultimately, advertisers are following eyeballs. They are trying to reach people wherever they are.”).

There are two ways to pursue this ROI:

More engaging content

More influence over buying decisions

The rise of e-commerce advertising epitomizes the latter. Amazon, for example, is the closest platform to consumer buying decisions. By owning the distribution network of buying, they can auction off the most valuable attention in the world: those who are willing to buy.

One of the beauties of Google’s business model is that users come with intent to the platform, they know what they’re looking for. Amazon supercharges that by its proximity to the purchase.

For as long as Amazon has the ability to influence buying decisions, their advertising business will do well.

As we consider the potential for advertising in LLMs, they can combine the information search of Google, user data like social media, and (in the future) purchase proximity data from Amazon.

I’ll call out that OpenAI is reportedly working on a native integration to Shopify to allow you to check out from ChatGPT. Take that for what you will.

Trend #3: The Shift from Social Media to Media

The other avenue for improved ROI is more engaging content, and this has led to the decline of “social” media.

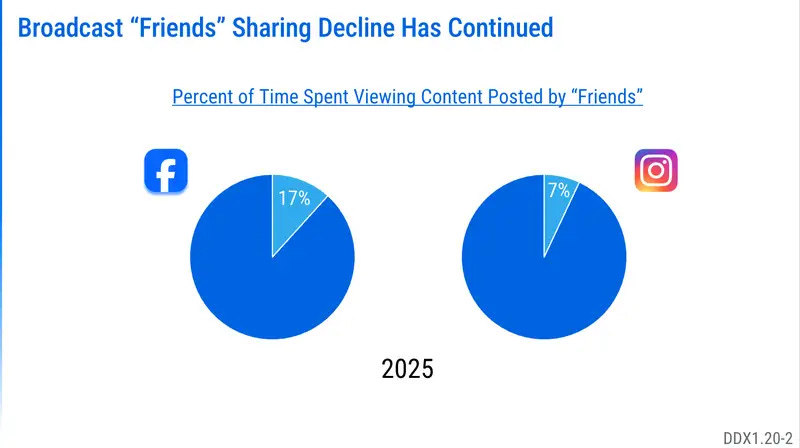

Perhaps the most interesting data point of the last few months came from Meta’s slide on the shifting of user behavior on social media:

This transition was pioneered by Tiktok, which has benefited massively from it. According to Sacra, ByteDance generated $146B in 2024 revenue, of which $34B came from Tiktok.

And at the expense of Meta. See a few quotes here from the recent trials:

Facebook’s and Instagram’s share of the amount of time people spend on social media apps has “gone down meaningfully,” Meta Platforms CEO Mark Zuckerberg testified on Wednesday,

“Friends and family sharing” was “less and less” a core way that people use Facebook.

He testified that TikTok is “bigger than either Facebook or Instagram,” while “people spend more time on YouTube than Facebook and Instagram combined.”

“TikTok’s growth so far is worrying and their trend-line projections have them overtaking Instagram in the US in terms of total [time spent] … TikTok in the US is a much bigger threat to our entire family of apps.”

On one hand, this shift from social media to media created an incredibly profitable opportunity for Tiktok and Meta. On the other hand, it creates an Innovator’s dilemma of sorts. The core job to be done of connecting people online is now unfilled, as the social media companies have pursued the most profitable activities.

It could be why Sam Altman’s serious about creating a social media component of OpenAI.

Perhaps this opens the door for another technology that can offer equivalent engagement and a social component. (This sounds a lot like Meta’s vision for the metaverse). *Hey Siri, remind me to write an article about the metaverse and technology realization times.*

Trend #4: The Shifting of Attention in Search

Conveniently, these trends all align with a few observations:

Advertising is harder than ever, leading to demand for new advertising channels.

Advertisers will pay most for the actual ability to influence buying decisions.

At the same time, the way we search for information is fundamentally shifting.

The opportunity for LLMs and advertisements creates both an incredible opportunity and an incredible conundrum. And one that creates perhaps the most interesting debate in the history of this industry. We’ll see that debate play out over the coming years, and it’s worth understanding deeply.

Attention -> valuable data -> influence -> revenue.

In other words, attention is all you need, and attention is shifting.

As always, thanks for reading!

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Investors should do their own due diligence before investing in any securities discussed in this article. While I strive for accuracy, I can’t guarantee the accuracy or reliability of this information. This article is based on my opinions and should be considered as such, not a point of fact. Views expressed in posts and other content linked on this website or posted to social media and other platforms are my own and are not the views of Felicis Ventures Management Company, LLC.

Great Explainer!

I wrote this wayy back. When you do cover the Metaverse, would love your opinions on this- https://codinginterviewsmadesimple.substack.com/p/the-metaverse-is-a-good-business?utm_source=publication-search