On the Lifecycle of Industries

Two Roads Diverge: AI's Rise and Software's Consolidation

This feels like an especially interesting time to be investing in technology (maybe it always feels this way!) As I teed up last week, perhaps the most important question in AI markets is where we’re at in this industry’s lifecycle.

It brings up a more important point altogether: how should we think about investing throughout the lifecycle of an industry? How should we think about investing in companies in new industries vs old ones? For a fun example of the game we play: if OpenAI were to IPO at the $300B reported valuation of their next round, they’d be worth just less than Bank of America (roots trace back to 1784!) and right above Wells Fargo (founded 1852!).

Summarized, the question I’m asking is: What’s a good theory on the lifecycle of industries? As Charlie said:

What is elementary, worldly wisdom? Well, the first rule is that you can’t really know anything if you just remember isolated facts and try and bang ’em back. If the facts don’t hang together on a latticework of theory, you don’t have them in a usable form.

Consider this my humble attempt at a theory on the lifecycle of industries.

I think it’s particularly relevant today as we’re simultaneously witnessing the rapid growth of AI and the slow descent of enterprise software growth rates:

My goal of this article is to answer a few questions:

What is a good general theory on the evolution of industries?

How do companies differentiate and succeed in the early stages of an industry lifecycle?

Who benefits as industries mature and start to consolidate?

A spoiler: it’s a lot like my middle school basketball coaches telling me how to defend big guys: Do your work early.

A Brief Intro to the Lifecycle of Industries

One theory I particularly like on the evolution of industries, which comes from Steven Klepper and Michael Gort, lays out five stages of the industry lifecycle:

Birth - Introduction of a new product by its first producer.

Expansion - Sharp increase in the number of producers.

Peak - Number of entrants approximately equals number of exits.

Consolidation - Negative net entries into the industry.

Equilibrium - Small number of producers continue until an industry dies or is reinvented.

Those early days of an industry is where I’ll start.

Industry Birth = Problems to Be Solved

Michael Mauboussin, in “New Business Boom and Bust,” laid out a wonderful analogy comparing the development of the human brain to the development of new industries.

As a child’s brain develops, it creates far more neurons than are actually necessary, laying the pathways for all the potential neural pathways that may be used. As the brain determines what pathways will actually be used, it “prunes” the unused pathways:

As new industries develop, products flood the market, providing many potential solutions to customer problems.

The “market,” or the aggregate demand from all customers, then selects the products or services that best solve their problems.

For a new industry like AI, we’re just starting to see the market select its preferred solutions.

Now, the question becomes, how do you differentiate in these early cycles?

Differentiation in the Early Stages of Industry Lifecycles

The earlier you compound feedback cycles, the faster you compound. This is why first-mover advantage matters so much.

The earliest producers get to pick the lowest-hanging fruit, the easiest problems to solve. They get the “king-of-the-hill” position on all those customers, which puts the burden on competitors to provide enough performance improvement to convince customers to switch.

It also creates positive feedback loops: get data on customer needs, develop products for customers, build relationships, and get more data on customer needs. At the same time, a company’s reputation compounds, revenue grows, and companies can raise more capital, which further allows companies to solve customer problems.

This is particularly important in network effect businesses. It’s not a guarantee you’ll win the market; you might take the wrong strategy and get beaten by a superior approach later on (i.e. Google showing up late to the search party). But you’d rather be in pole position.

How else can companies differentiate?

Verticalization & Domain Expertise: The better a company understands the unique problems of an industry, the better they can solve those problems.

Distribution Networks: Companies with existing distribution networks can release products and upsell them to existing customers rapidly (also adding to the speed-to-market point).

Data Advantages: Proprietary data leads to proprietary insights, whether accessed through partnerships, integrations, or experiments.

The X factor of finding ways to solve customers problems: At an event last year, I heard David Senra tell a story about Fastenal, who sells an entirely commoditized product: quite literally nuts and bolts. Somehow, they had 4x the margins as competitors and were still gaining market share. They did that by having the best customer service on the planet. Their founders were obsessed with customer experience; they went out of their way to show customers that, and they dominated a market by doing it.

And a reminder from Jensen: "My will to survive exceeds almost everybody else's will to kill me."

Depending on these variables, the market starts to “select winners” and those winners start their Power Law compounding. The rate of competitor entry slows, until eventually hitting its peak.

Industry “Peak” & Maturation

The peak of an industry lifecycle is defined as the point at which the number of companies exiting (acquisition, bankruptcy, etc.) equals the number of companies being founded.

This is particularly hard to measure for software-based industries because the capital requirements to start and run a software business are so low. This leads to the constant influx of companies and few exits of companies.

So rather than definitively saying “SaaS is consolidating,” I’ll say that it’s clear the growth of the industry is slowing.

One of the side effects of this growth decline is the rise of “zombies” in private markets: companies that aren’t large enough to draw interest from investors but aren’t profitable enough to draw interest of acquirers.

As described by Jamin Ball, “A zombie is a company that (in it’s current form) is not attractive to public markets or acquirers. There are so many companies sitting in the $50m - $300m ARR range, growing <20%, and burning money or barely breakeven.”

For context, see the total unicorns created and their ensuing “down rounds” (raising money at lower valuations) below:

Who benefits when industries consolidate?

Oftentimes, industry consolidation creates something like a Golden Age for industry leaders. The number of competitors dwindles as the industry grows.

The perfect scenario is a company that has strong competitive advantages, barriers to entry, a growing industry, and competitors that are “donating share.”

Now, at this point, your hackles might be raised, and you say, “Eric, there are no free lunches in investing; when have we seen that happen?”

Well, look, it is rare! But this is the story of many of the largest tech companies today:

Spot a company benefitting from the Power Law in an industry with winner-take-most dynamics.

Spot an industry that’s going to grow larger and for longer than everyone thinks.

An early monopoly on a rapidly growing industry creates a recipe for winners in technology.

Let’s take the semiconductor industry for example:

In the semiconductor industry, there have only been a few public semiconductor companies founded since 2000. A few others have been spun off or created out of mergers. But the vast majority of companies were founded between 1970 and 2000:

Yet the industry has nearly 3xed revenue in that period, with almost no new companies, from $222B in 2000 to $626B in 2024.

Now, the barriers to entry in semiconductors are massive which has made this more pronounced than most industries. But the point stands.

While it’s common in technology, not all industries trend towards consolidation. Even if they do, that doesn’t mean profits accrue there. Take airlines for example; the industry is relatively consolidated but those businesses are infamously challenging to run.

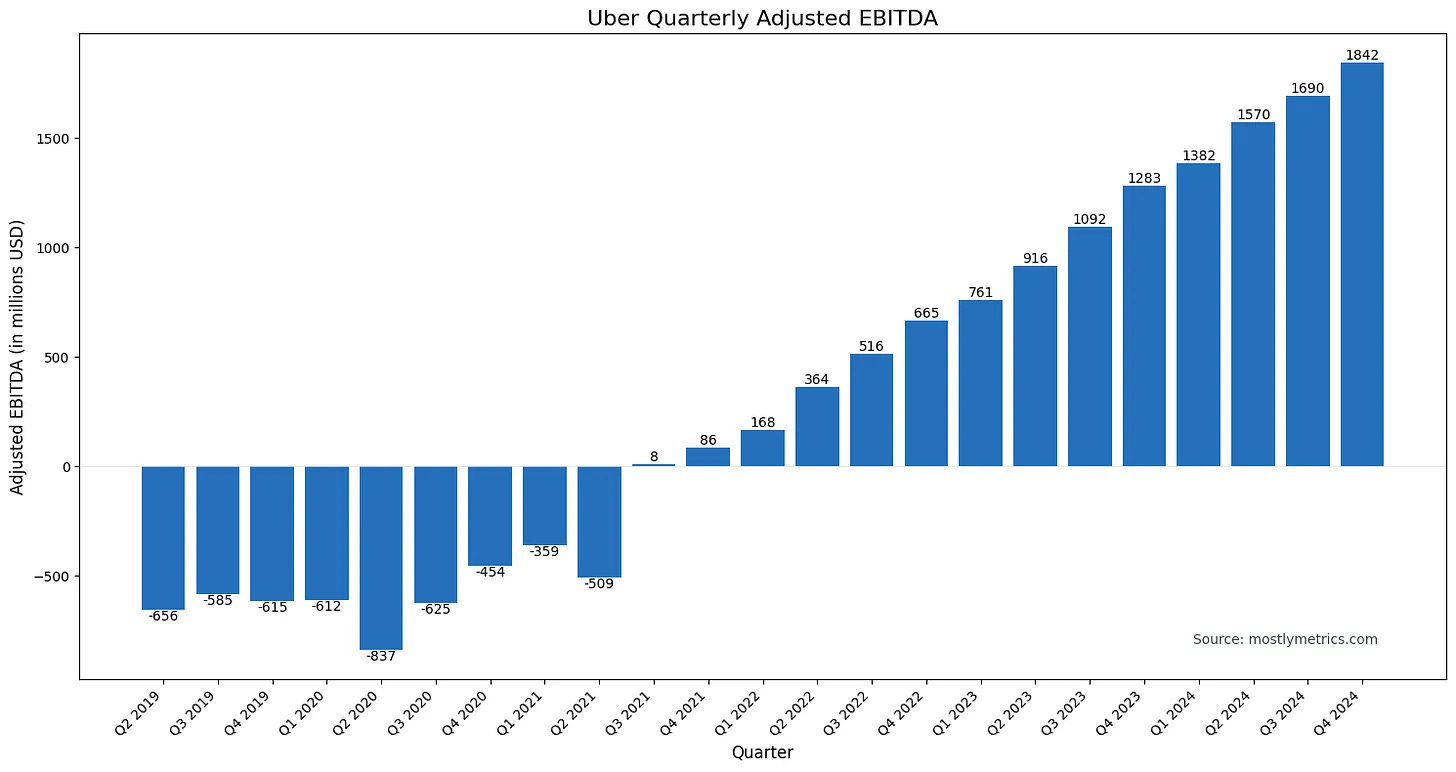

One final point: “broken economics” may start to sort themselves out, such as in railroads or even recently in ride-sharing. Natural monopolies lend themselves towards these outcomes, requiring huge upfront capital expenditures on the front end but monopolistic profits on the backend.

See Uber’s economics over the last five years here:

Then, as the industry stagnates, competition decreases, innovation slows, and more problems arise that need to be solved. And so goes the industry lifecycle.

Why this time is (a little bit) different:

If you’re looking for me to predict the next 12 months in AI or “where we’re at in the cycle,” I'm sorry to disappoint!

As I said in my annual letter, “I’m afraid I don’t have the foresight or the inclination to predict what will happen in technology or markets over the next 12 months (and I can’t imagine anyone else wants that!).”

What I will say is this: one fascinating observation is that industry lifecycles seem to be compressing, meaning industries rise and consolidate faster than before.

In software-dominated fields, this is only reasonable. First, software products iterate much faster. Second, they’re iterating faster and faster via the advancements in AI coding tools. Third, product market fit can be found faster because of the faster dispersion of information. Social media allows good companies to find their customers and hear their feedback faster than ever!

Additionally, and specifically to AI, enterprises are clamoring to adopt AI. Every organization I talk to is interested in adopting AI.

Combined, we have faster product development times (more neurons created to explore potential paths of “product-market fit”) + faster positive feedback loops (neurons are used earlier and paths are hardened faster) + more eager customers = compressing of early industry lifecycles.

The implication of that is this: Positive feedback loops are faster. Power Law winners emerge faster. Strike while the iron’s hot, but chasing others’ successes may be more dangerous now than ever.

As always, thanks for reading!

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Investors should do their own due diligence before investing in any securities discussed in this article. While I strive for accuracy, I can’t guarantee the accuracy or reliability of this information. This article is based on my opinions and should be considered as such, not a point of fact. Views expressed in posts and other content linked on this website or posted to social media and other platforms are my own and are not the views of Felicis Ventures Management Company, LLC.

Great article on overall trends. How do you think ai first approach will change the rules of entering into traditional industries for new companies?

This article also brings up a very interesting point about consolidation and barriers to entry once the industry matures?

What causes breaks in this industry? Would be very interesting to study.

Another note- what about "smaller fish" that come in to solve specific problems for a mature space. For example an error correction startup for Quantum Computing or the AI Safety startups for Gen AI. What sets them up for winning? How does one pick winners there? Would love to hear your thoughts on that.