The Hyperscalers & The Compute Crunch (Quarterly Update)

Coding agents push the compute ecosystem to its limit

Most of these cloud updates start with a market share update, or perhaps updated revenue from the hyperscalers, or even a graph of CapEx continuing to go up and to the right.

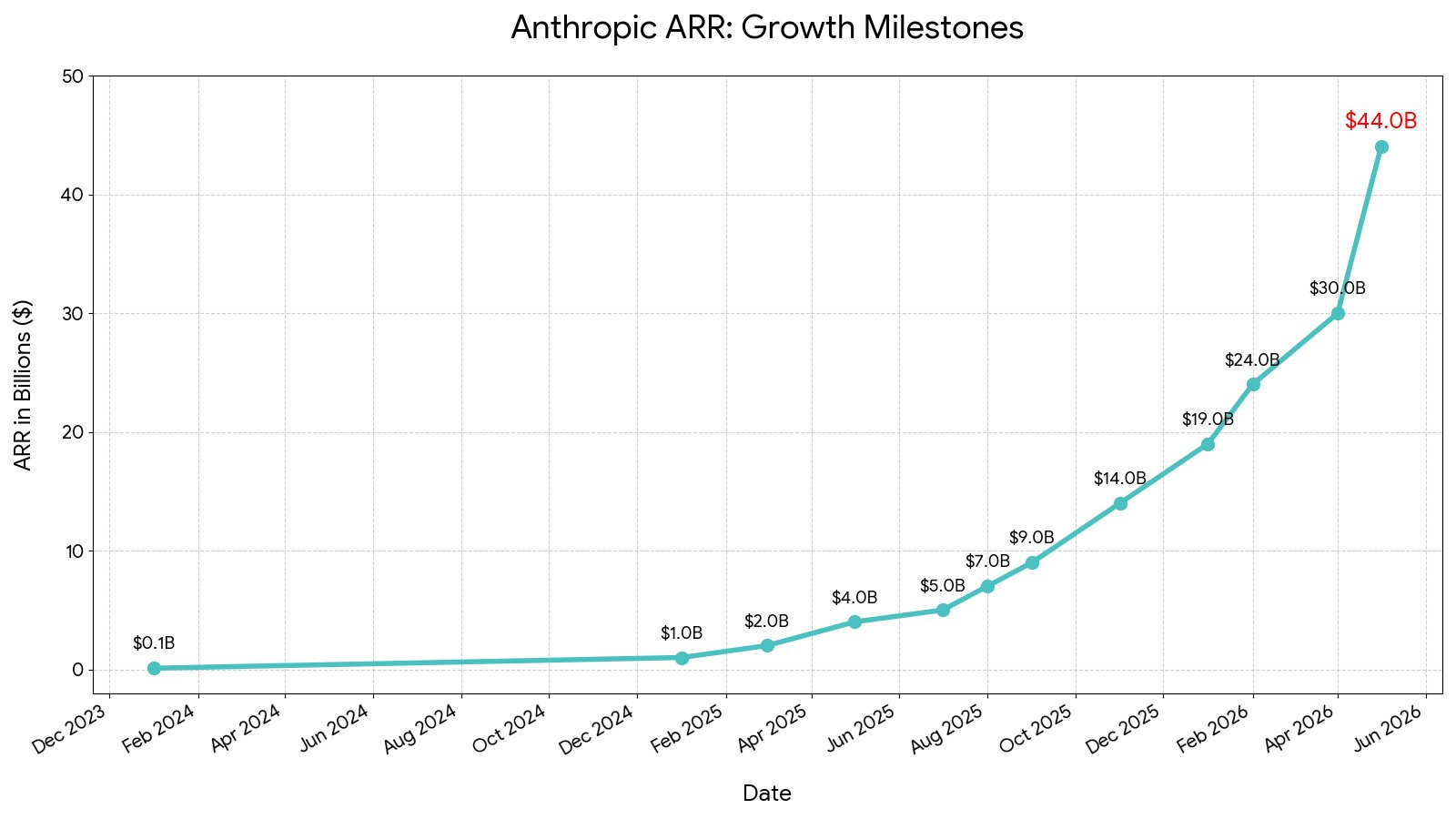

However, this one will start with another chart. That of Anthropic’s revenue:

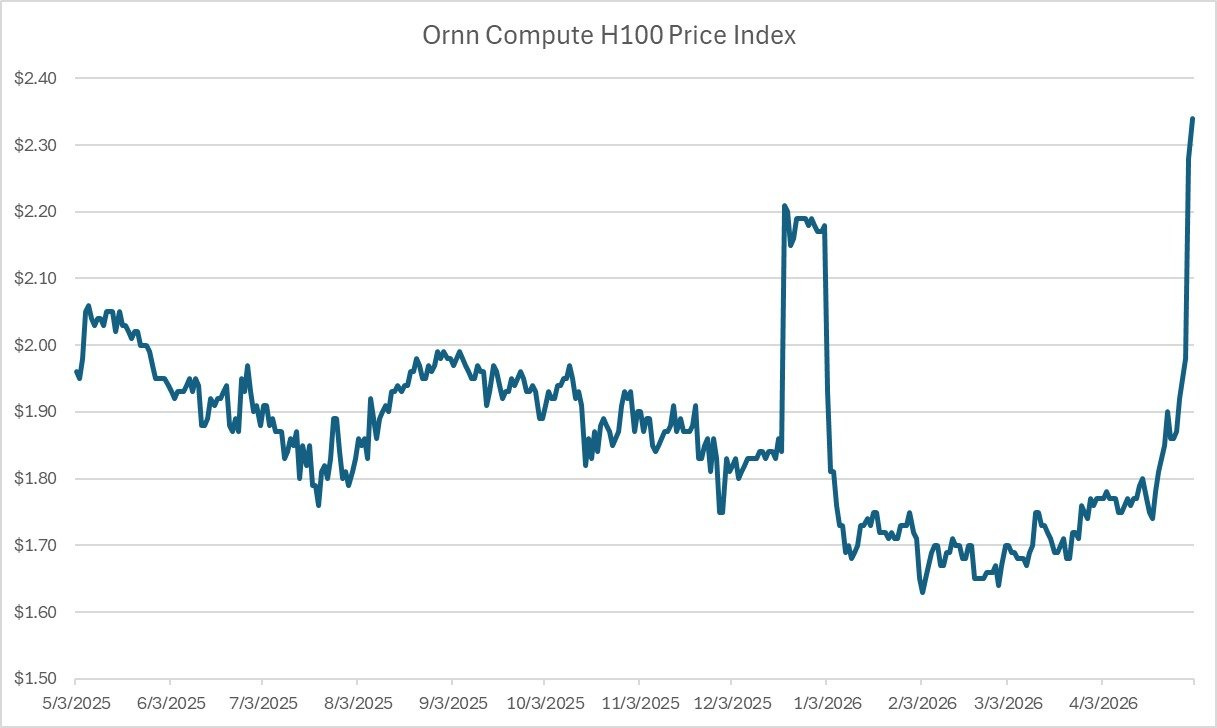

The talk of the town for the last ~18 months has been about agents (LLM-based tools that can autonomously complete work without human oversight). But finally, over the last quarter, that hype became reality. We saw autonomous coding agents (primarily via Claude Code) go mainstream and, in doing so, push the broader compute ecosystem to its limits. H100 rental prices are now the highest they’ve been in 52 weeks:

Well, given the hyperscalers’ position in between supply (hardware) and demand (AI applications), this led to one of the more interesting quarters in recent history:

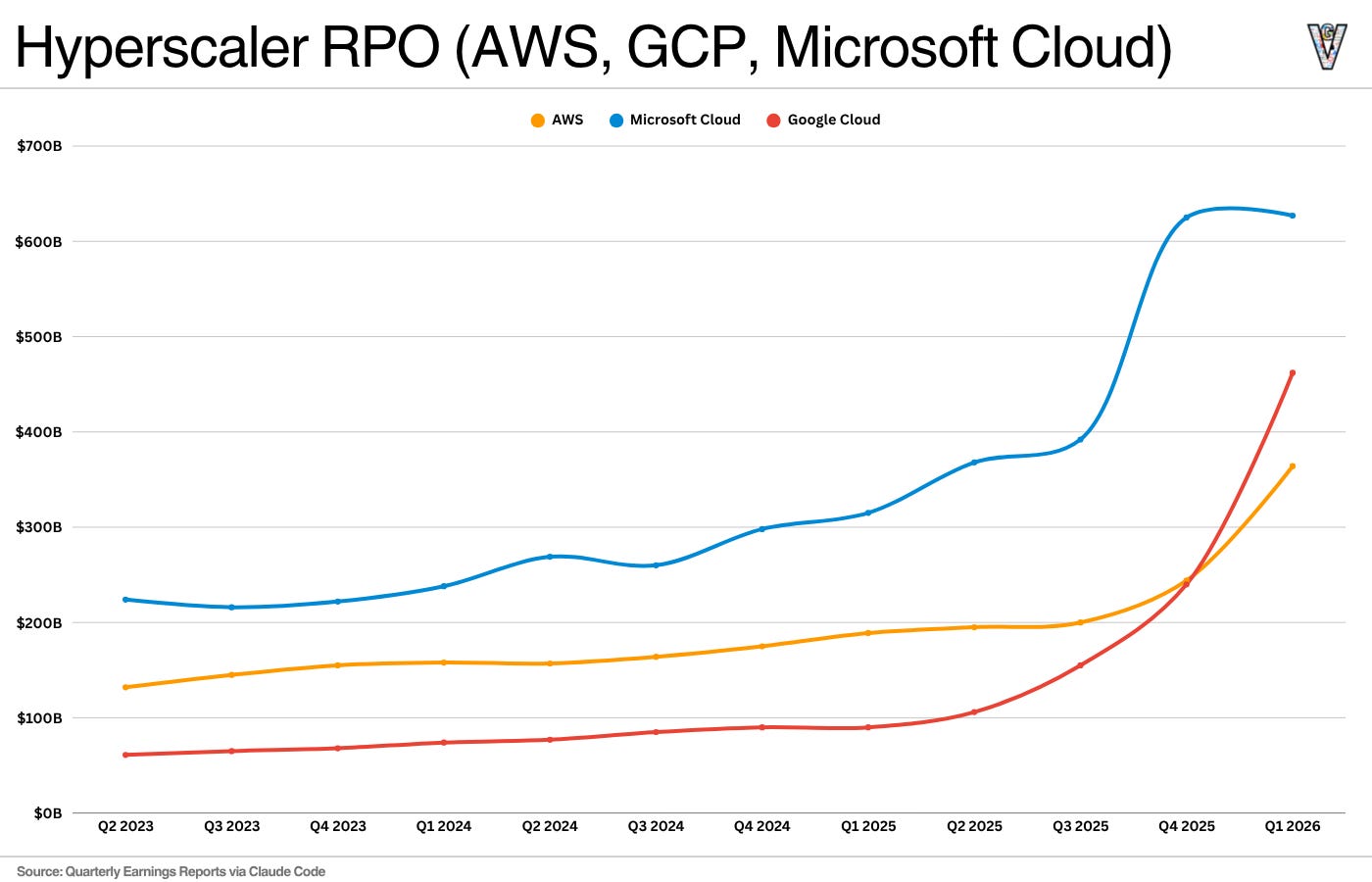

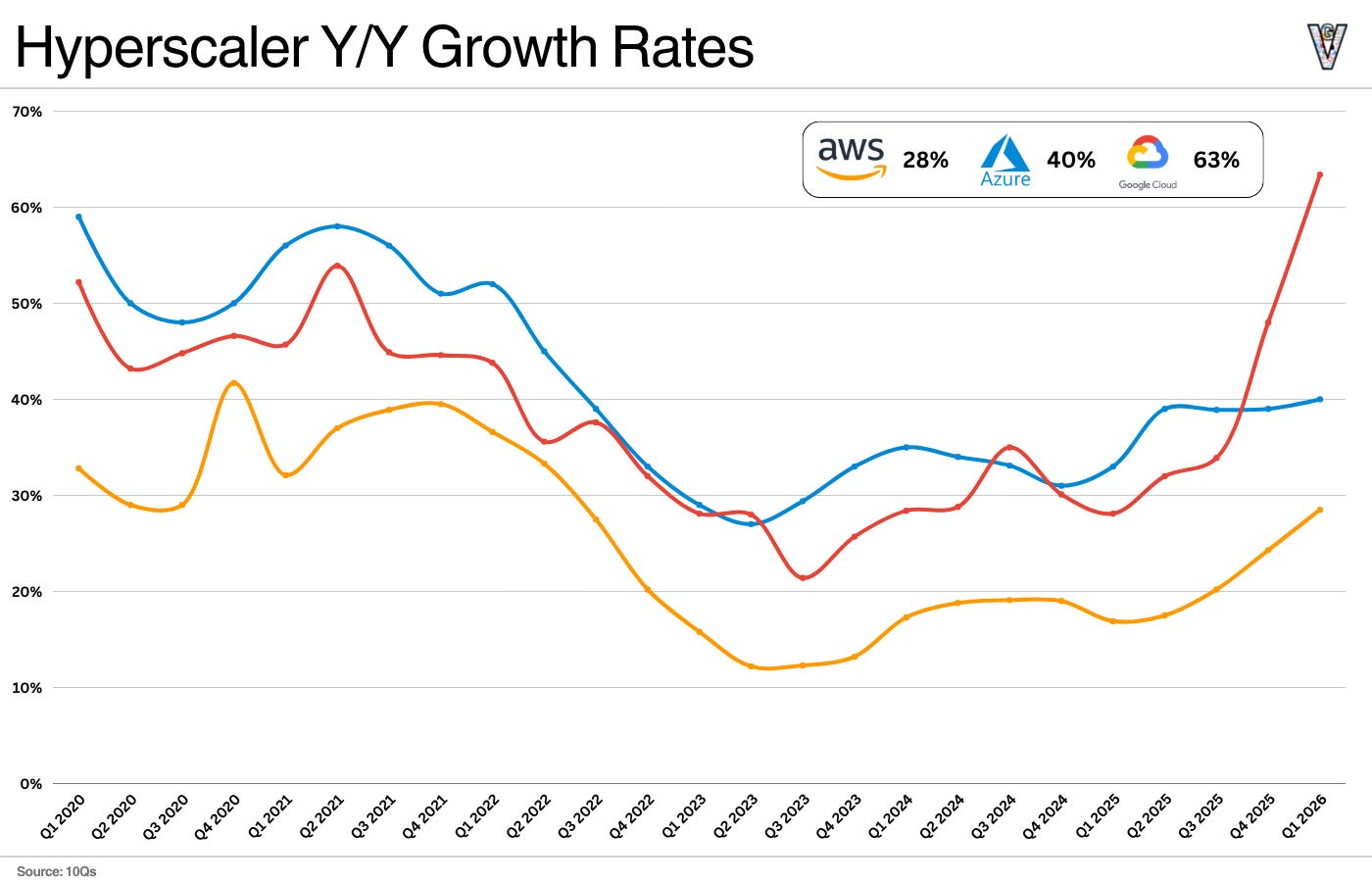

Azure revenue growth 40%, RPO growth of 99% Y/Y

GCP growth 63%, RPO growth of ~2x QoQ (to $462B)

AWS growth 28%, RPO growth of ~93% YoY (to $364B)

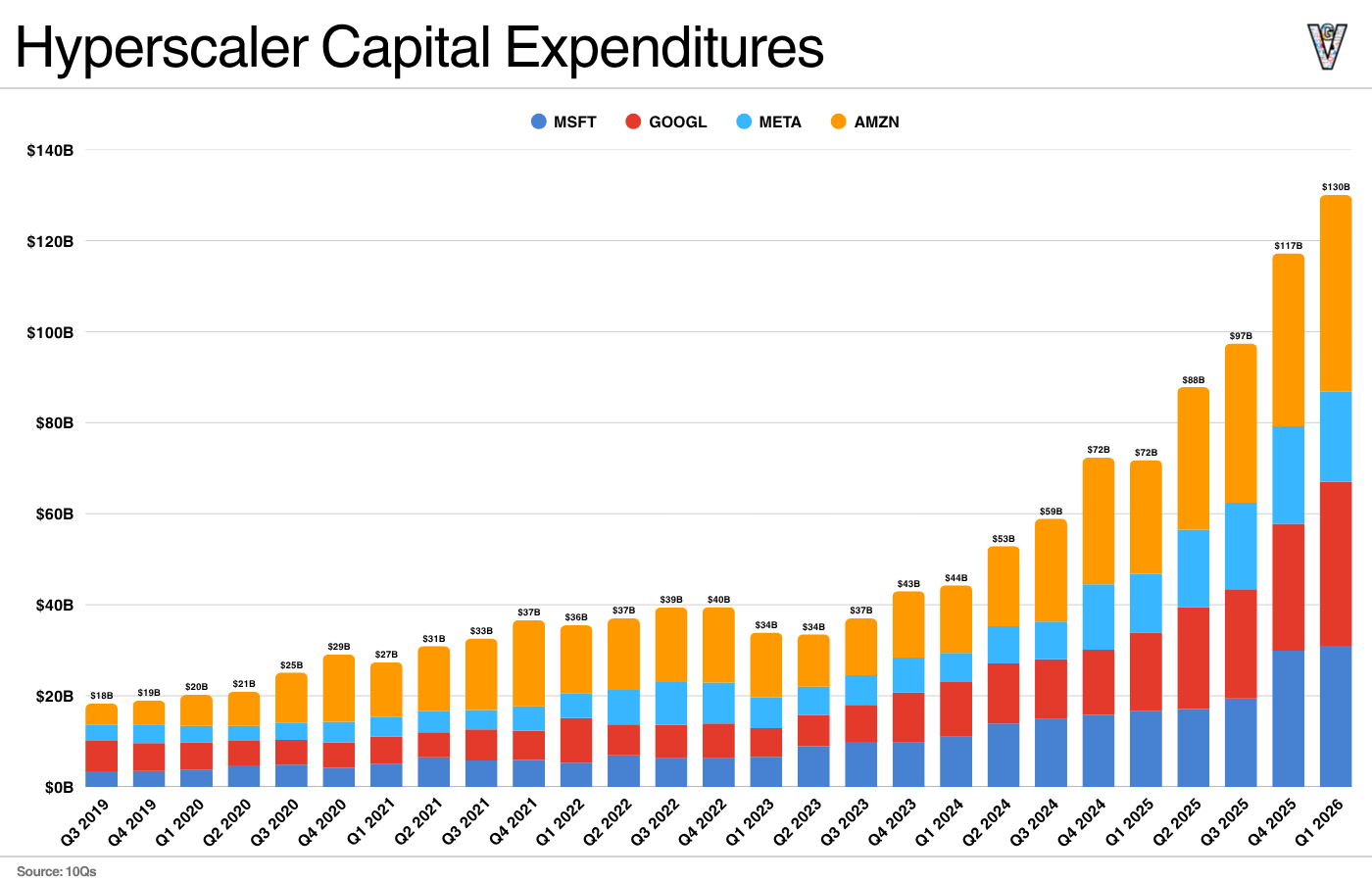

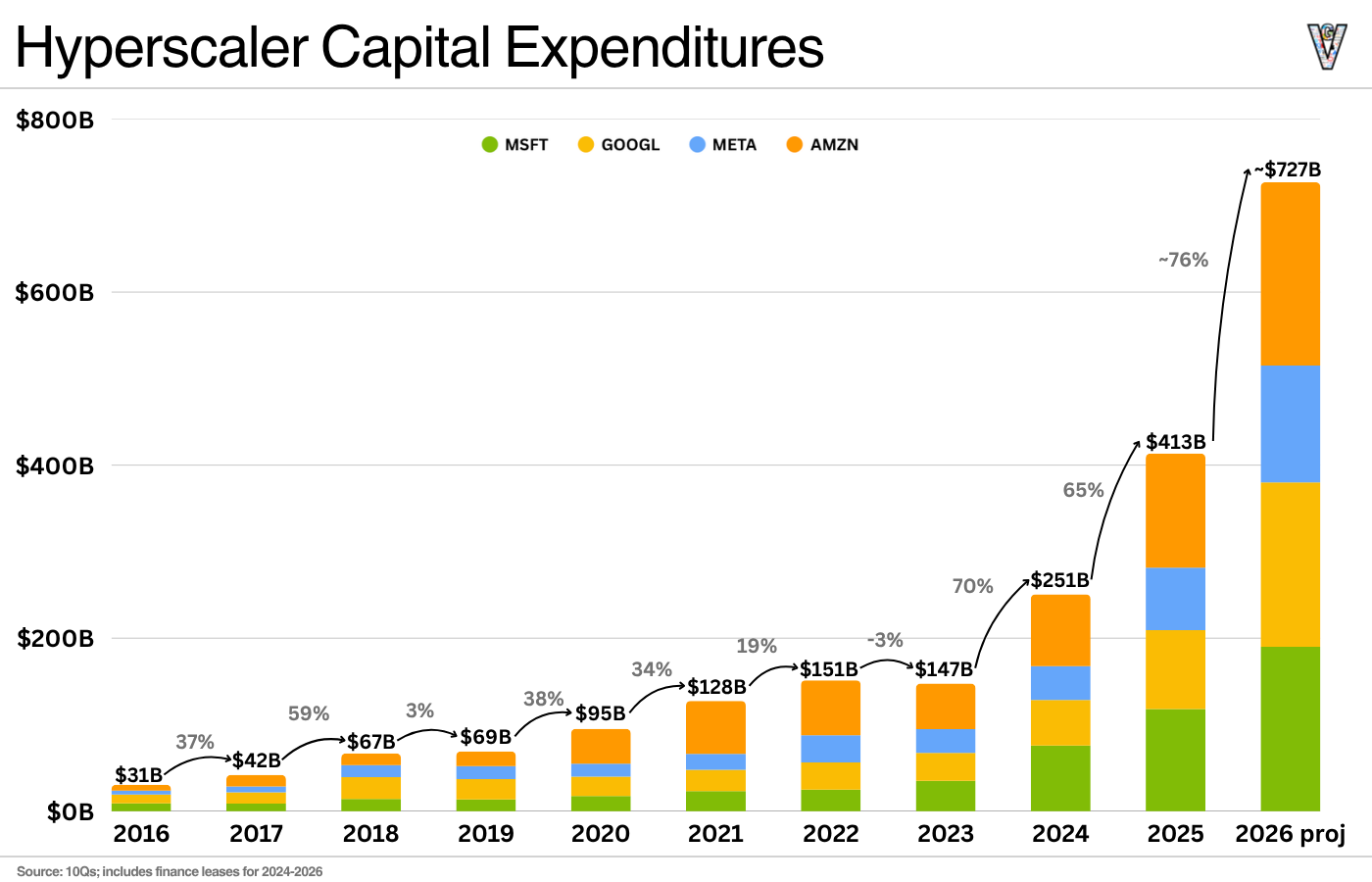

CapEx projected to be $700B+ between Microsoft, Google, Amazon, and Meta in 2026; and accelerating in 2027

Perhaps most interesting, the feeling for a while was that we were getting closer to a supply/demand equilibrium. But this quarter, the cloud providers hinted that the supply/demand gap widened.

Which means more CapEx, more investments in data centers, chips, networking, storage, and energy. In other words, the AI buildout shows no signs of slowing.

The Current State of Hyperscaler CapEx and the Compute Crunch

The hyperscalers are the primary middlemen delivering compute in the AI boom. They sit between supply and demand, which means they give us the best insight into where the supply/demand equilibrium actually stands.

Both their qualitative and quantitative commentary this quarter told the same story that demand far exceeds supply. See the CapEx numbers below, with this quarter’s CapEx surpassing $130B, up 80% from the same quarter last year:

On the qualitative side, Google, Amazon, and Microsoft all signaled they’re going to meaningfully increase CapEx in 2027. Demand is outpacing supply, and they don’t see that changing:

“When the TAM is so expansive and when shortages are generally growing between supply and demand, it gives you a lot of confidence in the ROI—certainly starting with the platform side.” — Amy Hood, Microsoft Q3 FY2026

“Strong customer demand across workloads, customer segments, and geographic regions continues to exceed available capacity. Even with these additional investments and continued efforts to bring GPU, CPU, and storage capacity online faster, we expect to remain constrained at least through 2026.“ — Satya Nadella, Microsoft Q3 FY2026

“We are compute constrained in the near term. And as an example, our cloud revenue would have been higher if we were able to meet the demand.” — Sundar Pichai, Alphabet Q1 2026

“The cost of components, particularly memory, has skyrocketed. We are in a stage where there is just not enough capacity for the amount of demand.” — Andy Jassy, Amazon Q1 2026

And again, the remaining performance obligations (RPO) numbers suggest demand is growing faster than supply:

The obvious callout here is Google growing its RPO roughly 5x Y/Y, and doubling Q/Q. This kind of acceleration is remarkable.

Right now, whoever can bring capacity online will generate revenue from it. I think Google’s growth comes down to two things: Google has one of the strongest data center infrastructure teams in the world, and they have the most advanced internal silicon program on the planet. Their TPUs give them another lever of compute availability that the other vendors can’t match (even though, AWS’ chips are doing very well, the program is not as mature as TPUs yet).

That’s likely what’s enabling them to sign these huge contracts with AI labs, who are the most important compute customers in the world right now. And as a result, increase their RPO faster than their competitors.

In summary:

All three hyperscalers are massively compute-constrained right now

Whoever can bring compute online the fastest will generate revenue from it

Relative to the size of their cloud business, Google is outperforming in their ability to bring compute online

All three of these points are being reflected in short-term numbers.

Updated Metrics & Market Share

Just to emphasize how strong GCP’s quarter was, see below for Y/Y growth rates from the hyperscalers:

They’ve accelerated their growth rate in two quarters from mid-30s percent to mid-60s percent. AWS & Azure also had great quarters: AWS accelerated revenue for the fourth quarter in a row, surpassing $150B run rate. Microsoft called out that their AI run rate surpassed $37B.

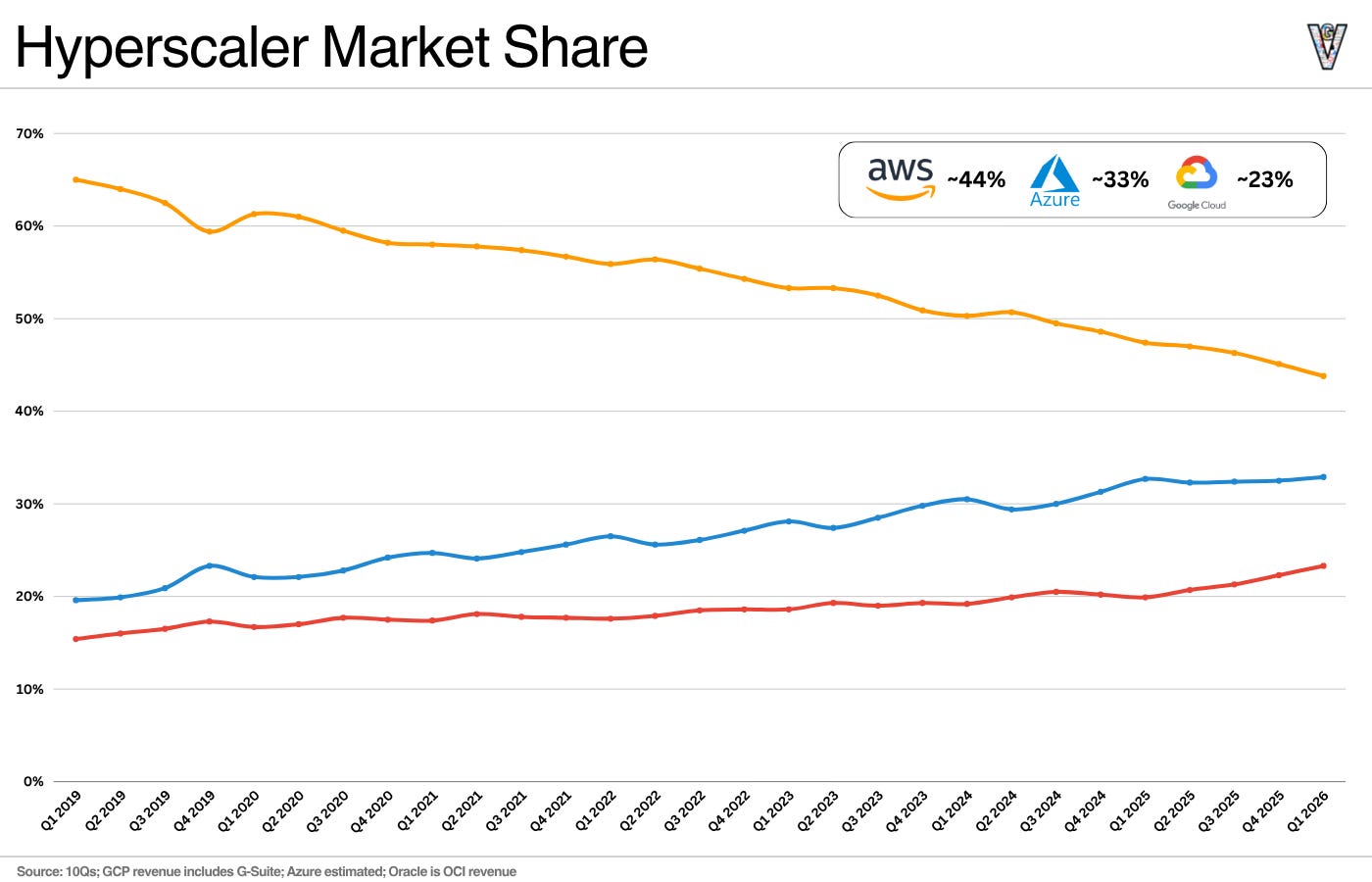

If we look at the estimated market share between the three vendors, Azure and GCP continued to make up ground:

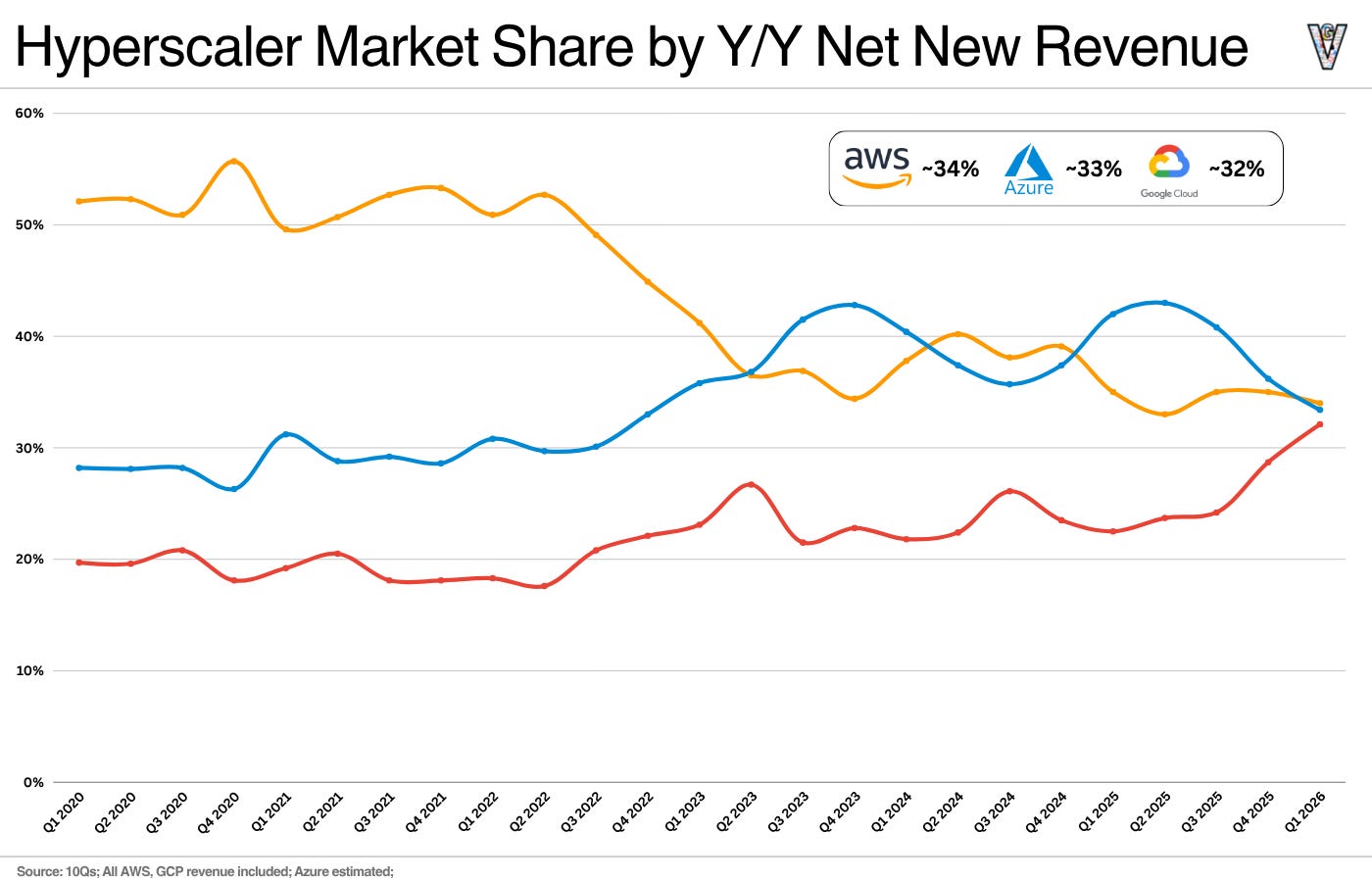

But the more interesting way to view market share is based on the percentage of net new revenue over the last four quarters that each vendor generated. This gives us a sense of “market share momentum.”

If you look at net new revenue generated over the last four quarters, it’s basically an equal three-horse race between AWS, Azure, and GCP. GCP has been a clear third-place player throughout the history of the cloud, and now, with their speed in bringing compute online, they’ve moved into a near three-way tie. Pretty incredible.

Where do we go from here?

All the qualitative and quantitative commentary would suggest we’re not slowing down.

The rise of AI coding agents gave us the first real examples of autonomous agents doing knowledge work at scale. And it pushed the compute ecosystem to its max capacity. CapEx will jump roughly 75% this year, and the hyperscalers suggested it would increase further in 2027:

Just how the AI coding boom had been building for 4+ years, and the explosion STILL surprised everyone; I suspect other use cases will follow a similar path. And if additional agentic use cases go mainstream outside of coding, that compute crunch will get worse before it gets better.

For the time being at least, seems the infrastructure boom will keep on rolling!

As always, thanks for reading!

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Investors should do their own due diligence before investing in any securities discussed in this article. While I strive for accuracy, I can’t guarantee the accuracy or reliability of this information. This article is based on my opinions and should be considered as such, not a point of fact. Views expressed in posts and other content linked on this website or posted to social media and other platforms are my own and are not the views of Felicis Ventures Management Company, LLC.

Makes me think: anyone that can drive down compute usage will likely permanently drive the hyper scaler where they operate to another level.

Theoretically if you had a solution to do that, would you rather sell to hyper scaler or sell to the apps companies hosted on them?