Q1 '25 Cloud Update: Risk-Adjusted AI

A Quarterly Cloud Update on Amazon, Microsoft, Google, and Meta

Hyperscalers sit at the center of the AI ecosystem, both as compute distributors and as the ones funding the largest computing infrastructure buildout in history.

Because of this, they give us a perspective into AI markets that no one else can. It’s why I’m so fascinated by the game theory of their decision making, and why I write a quarterly update on their businesses: investment strategy, market share updates, and growth rates. Let’s get to it.

The Game Theory of Hyperscalers’ AI Investments

Given that AI seems to be the driving force for accelerated computing needs over the next decade, the hyperscalers are as well-positioned as nearly anyone to benefit from AI. As AI makes humans more productive, they’ll “outsource” their labor to computers.

As AI coding tools further decrease the barrier to entry to software, more and more software will be built. We’ll only get more compute-hungry, and the hyperscalers couldn’t be happier.

Because of this, they’ve fully pursued AI, pouring hundreds of billions into infrastructure investments.

As I laid out last year, this was logical:

The equation for hyperscalers is relatively simple: data centers are at least 15-year investments. They are betting compute demand will be higher in 15 years (not a crazy assumption).

If they do not secure these natural resources, three things could happen:

They will lose business to competitors who have capacity.

They’ll have to secure sub-optimal land with worse price/performance profiles.

Challengers will buy this land and power capacity and attempt to encroach on the hyperscalers.

If they secure this land and don’t need the computing power right away, then they’ll wait to build out the “kit” inside the data center until that demand is ready. They might’ve spent tens of billions of dollars a few years too early, and that’s not ideal. However, the three big cloud providers have a combined revenue run rate of $225B+.

As Google’s CEO Sundar said, “The risk of under-investing is higher than the risk of over-investing.”

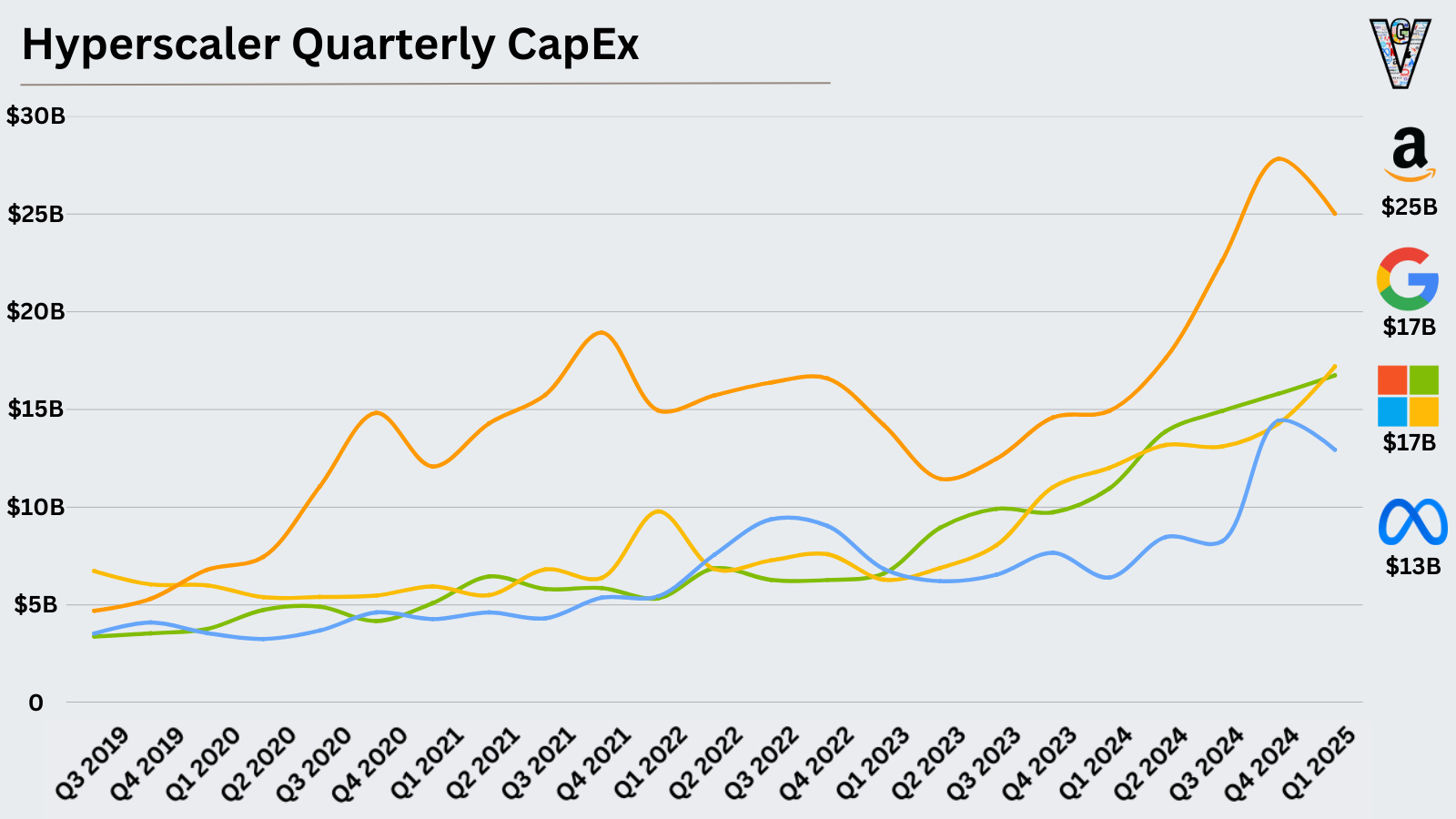

However, for the first time, we’re hearing reports of these investments slowing down.

In part, this is simple downside limitation. If demand constricts, they won’t be exposed to tens of billions worth of idle compute.

However, the more interesting part is that they’re adjusting investments based on “the shape of workloads” moving forward. As Satya said:

“The reality is we've always been making adjustments to build, lease, what pace we build all through the last, whatever, 10, 15 years, it's just that you all pay a lot more attention to what we do quarter-over-quarter nowadays.

Having said that, the key thing for us is to have our builds and lease be positioned for what is the workload growth of the future, right?

You don't want to be upside down when the shape of demand changes because, after all, with essentially pre-training plus test time compute, that's a big change in terms of how you think about even what is training, right.”

I'll lay out a revised equation. The cloud providers still want to maximize upside from three areas:

AI inference (APIs, GPUaaS, etc.)

AI companies building on their platforms (just like AWS rose by supporting the early cloud software winners)

Their own AI products (The AI pie is still up for grabs)

Inference, as the enabler of applications, resembles the recurring SaaS revenue model of the last decade. The hyperscalers will do everything they can to power those applications.

Training, on the other hand, requires larger, upfront investments. As Zuck described, “I’d guess that in the next couple of years, the training runs are going to be on gigawatt clusters, and I just think that there will be consolidation.” These large-scale expenses present a less attractive risk-reward profile.

The last two years have come with a lack of clarity on the future of AI. In the absence of clarity, the biggest risk was underinvesting.

However, as the economics of AI come into focus and these infrastructure investments unlock AI applications, the hyperscalers can focus on investing in a future that provides them the best ROI per dollar deployed with the least risk of overinvestment. Risk-adjusted AI, if you will!

Updated Market Statistics

What does this mean? The hyperscalers are getting cautious, not in the short term, but in the long term. They haven’t changed their short-term spending meaningfully; if they do, it won’t be reflected immediately.

The good news is that they’ve got the money to invest. Combined, the three cloud providers are at a $247B run rate, growing 23.9% Y/Y.

A reminder on all of these numbers: the three cloud providers report different product lines in their “cloud” units. Azure just restated their numbers a few quarters ago, GCP includes Google Workspace. The numbers are all directionally correct, and precisely incorrect. Azure includes estimates of revenue based on public commentary.

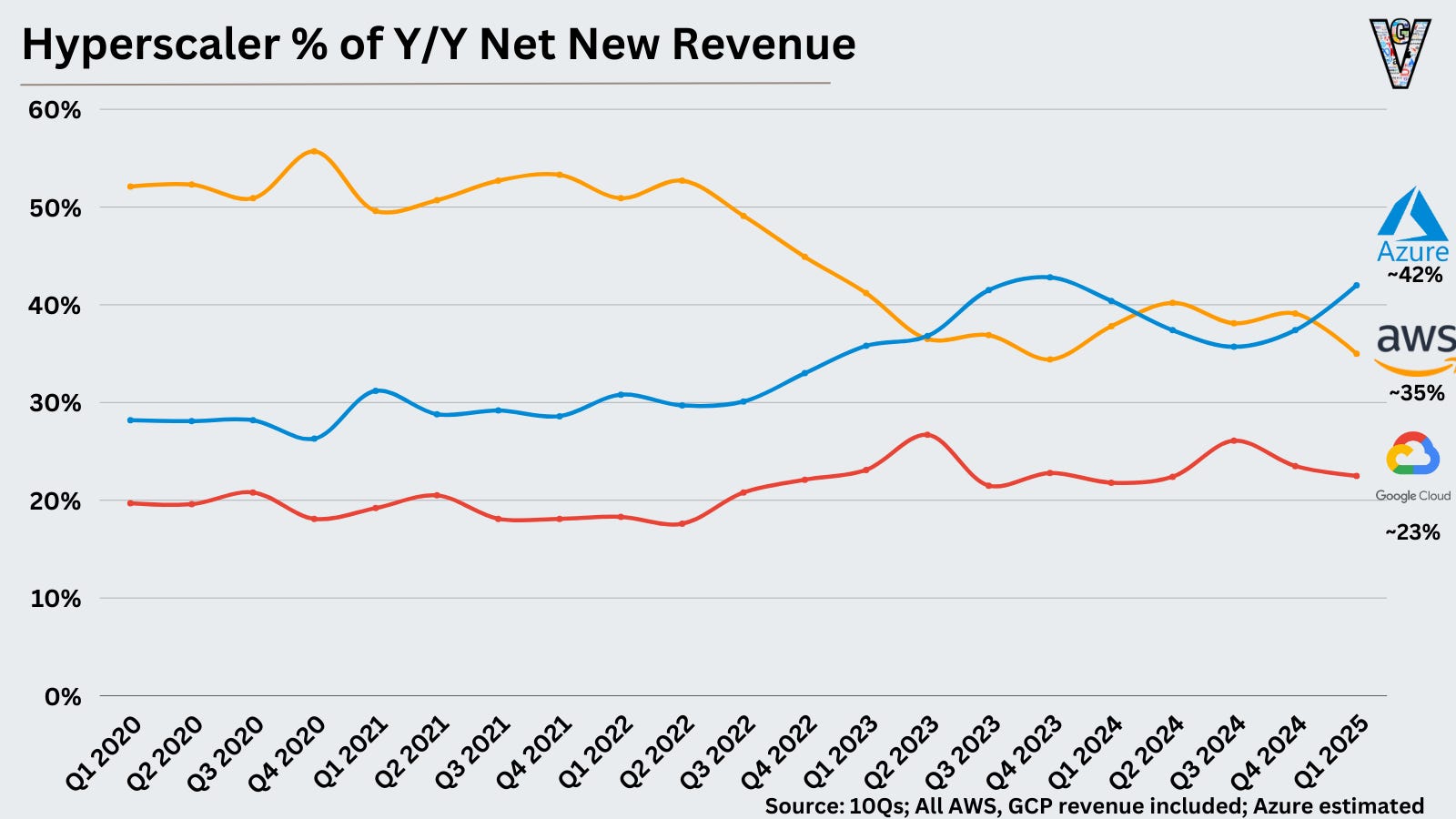

We can see updated (estimated) market share here:

And the more interesting way to view market share is what % of net new revenue generated over the last 12 months did each company capture:

Based on this, Azure has had a few very strong quarters, perhaps because of the OpenAI relationship.

I’ll end with one final stat (and one that Warren Buffett might find amusing). For all of the noise of the last 6 months, the average stock performance for Google, Amazon, and Microsoft is just about 0%.

There’s a lesson in that. Unfortunately for me, it may be to read fewer quarterly updates, and fewer updates in general. As Nick Sleep said, “We keep our discussions to as high a level as we can manage in the belief that, in the long run, the high level is all that matters.”

As always, thanks for reading!

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Investors should do their own due diligence before investing in any securities discussed in this article. While I strive for accuracy, I can’t guarantee the accuracy or reliability of this information. This article is based on my opinions and should be considered as such, not a point of fact. Views expressed in posts and other content linked on this website or posted to social media and other platforms are my own and are not the views of Felicis Ventures Management Company, LLC.

Eric, these updates are great. I'm curious how you're estimate Azure revenue? Thanks